Natural capital should be valued for more than its market price. In this blog, Julia Wdowin and Diane Coyle argue that incorporating the social value of avoided carbon emissions provides a more complete way to estimate the value of wind as a renewable energy asset. They present a new methodology that supports the Beyond GDP agenda and could help strengthen natural capital accounting and policymaking as data and methods continue to evolve.

Renewable energy assets such as wind are playing an increasing role in powering the UK’s energy mix. Renewable energy is also central to meeting net-zero policy objectives. One key channel is through the reduction of carbon emissions emitted into the atmosphere. Reflecting their growing economic significance, several renewable energy resources, including wind, have been incorporated into the asset boundary of the System of National Accounts 2025 (SNA 2025). It is therefore important to consider what the valuation of wind under the updated SNA captures and what it leaves out.

This is because the standard national accounting framework values the environmental resource of wind according to its contribution to economic production as recorded in the National Accounts, capturing only the benefits that enter the national accounting production boundaries. This approach excludes a range of wider social and environmental impacts associated with wind energy generation. Economists refer to these effects on others that are not reflected in market prices as externalities, and they can be both positive and negative.

Therefore, the value of wind energy recorded in natural capital accounts under the System of Environmental-Economic Accounting (SEEA), and now within the updated System of National Accounts, does not fully reflect its broader contribution to societal welfare. This highlights the distinction between market prices and shadow prices (social welfare values).

In a new ESCoE discussion paper, we present a measurement approach to valuing wind as a renewable energy asset, taking into account the value of a key associated positive externality: avoided carbon emissions in renewable energy production.

A shadow value approach to a renewable energy asset

The international ‘Beyond GDP’ research agenda seeks to expand national accounting beyond traditional economic measures, highlighting how different forms of capital contribute to social welfare. It not only emphasises the exclusion of ‘missing capitals’ – those conventionally not treated as capital assets in National Accounts but which provide important inputs into economic production – but also examines how asset valuation relates to society’s overall wellbeing, rather than just the welfare of individual asset owners as reflected in market prices. For natural capital, this is a central point in the 2021 Dasgupta Review on the Economics of Biodiversity: environmental assets are systematically undervalued because market prices fail to reflect their true contribution to human wellbeing and long-run prosperity. Values that capture the broader contribution of capital assets to social welfare are the shadow values that we estimate in this paper (and which are explored conceptually in our 2025 ESCoE Discussion Paper).

Empirical estimation of the shadow value of wind

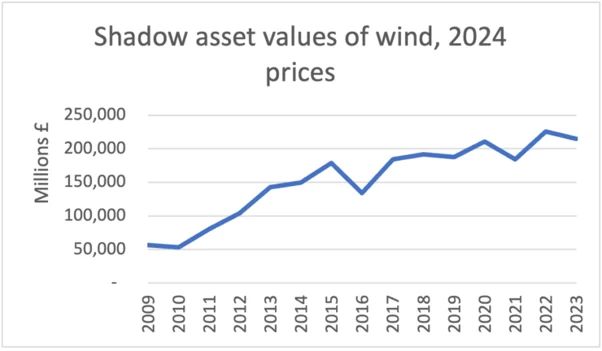

Our discussion paper estimates the annual shadow value of UK onshore wind as a renewable energy asset for 2009 and 2023, demonstrating a reproducible methodology for measuring shadow values of other capital assets. Once the value of avoided carbon emissions is considered, the estimates indicate that market price valuations of wind underestimate wind’s contribution to social welfare. Over these years, we find that the yearly asset value generally follows an increasing trend, but with greater variability across the second half of the time series. The annual asset values and time series trend are shown in Figure 1 below.

Figure 1: Shadow asset value estimates of wind, 2009-2023, mid carbon values.

Crucially, the estimates depend on a number of methodological choices discussed in the paper, for example, the choice of carbon value or social discount rate to use in calculations. For coherency, our methodology is consistent with many methodological choices made in UK Office for National Statistics (ONS) natural capital accounts.

Directions for future work

The paper considers the value of one important externality linked to wind in providing shadow value estimates but there are many more. It may be possible to value some in monetary terms such as estimating public health costs linked to reduced air pollution from the displacement of polluting fossil fuels. Other externalities may pose a greater challenge such as capturing the value of noise impacts from renewable energy generation. Although focusing on a single externality does not provide a comprehensive assessment of social welfare, the methodology demonstrates a feasible approach for statistical production and could be expanded in future to capture a wider range of social and environmental impacts, subject to data availability.

We might also consider the broader context in which associated externalities arise and which are likely not fully captured in market price equivalent valuations of wind. For instance, renewable energy sources are infinite and can be more stable sources of energy in the face of global oil supply shocks and global fossil fuel price volatility. Renewable energy can also support national security interests in this domain, reducing reliance on other countries in a fraught geopolitical climate.

Why valuing wind matters

The shadow asset value estimates suggest that conventional market-based valuations may underestimate the contribution of wind energy to social welfare. While the estimates incorporate the shadow value associated with avoided carbon emissions, they do not capture the full range of positive or negative externalities associated with wind used to provide renewable energy services. As a result, the values should be interpreted as conservative estimates of the broader societal benefits linked to wind as an economic asset.

If the value of renewable energy assets is systematically underestimated, investment incentives and policy decisions may not fully reflect their contribution to society. Incorporating externalities such as avoided carbon emissions into asset valuations can help align investment and policy more closely with broader social welfare and sustainability objectives.

More broadly, the methodology presented in the discussion paper demonstrates how national accounting can move beyond market prices to better reflect the value of natural capital. As data and methods continue to improve, extending this approach to capture a wider range of social and environmental impacts could support more comprehensive measures of economic progress and wellbeing.

Read the paper: The shadow value of wind as a renewable energy asset [opens on ESCoE website]

The views and opinions expressed in this post are those of the author(s) and not necessarily those of the Bennett School of Public Policy.